Jak kupować

Jak kupowaćDostawa

Doradca ds. zakupów

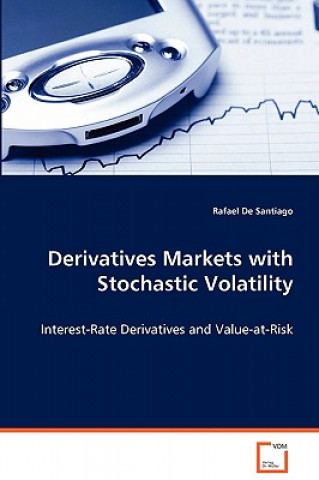

Derivatives Markets with Stochastic Volatility

Angielski

Angielski

199 b

199 b

30 dni na zwrot towaru

Mogłoby Cię także zainteresować

/

Twarda

/

Twarda

1 329.11

zł

1 329.11

zł

/

Miękka

331.82

zł

/

Miękka

331.82

zł

Although the assumption of constant volatility is areasonable approximation for some markets, in thelast two decades the need for more general non-constant volatility models has been the drivingforce behind numerous works in FinancialMathematics. In this book we study systems thatarise in interest-rate markets when the volatilityof the short rate is modeled as a function of twomean-reverting diffusions that vary on differentscales. This allows us to capturea rich variety ofvolatility patterns. In the last part of the bookthe analysis is extended to other areas, like Value-at-Risk, in which similar systems arise when thevolatility is modeled as a stochastic process. Thebook is oriented to researchers who work in thefield of Mathematical Finance, as well as topractitioners who would like to gain a betterunderstanding of how to include stochasticvolatility in their models.

Informacje o książce

Angielski